Korean J Lab Med.

2006 Dec;26(6):460-464. 10.3343/kjlm.2006.26.6.460.

Experience of a Break-Even Point Analysis for Make-or-Buy Decision

- Affiliations

-

- 1Department of Laboratoty Medicine, BoRyeong Asan Hospital, Boryeong, Korea. elimyh@naver.com

- KMID: 1889827

- DOI: http://doi.org/10.3343/kjlm.2006.26.6.460

Abstract

-

BACKGROUND: Cost containment through continuous quality improvement of medical service is

required in an age of a keen competition of the medical market. Laboratory managers should examine

the matters on make-or-buy decision periodically. On this occasion, a break-even point analysis

can be useful as an analyzing tool. In this study, cost accounting and break-even point (BEP) analysis

were performed in case that the immunoassay items showing a recent increase in order volume

were to be in-house made.

METHODS

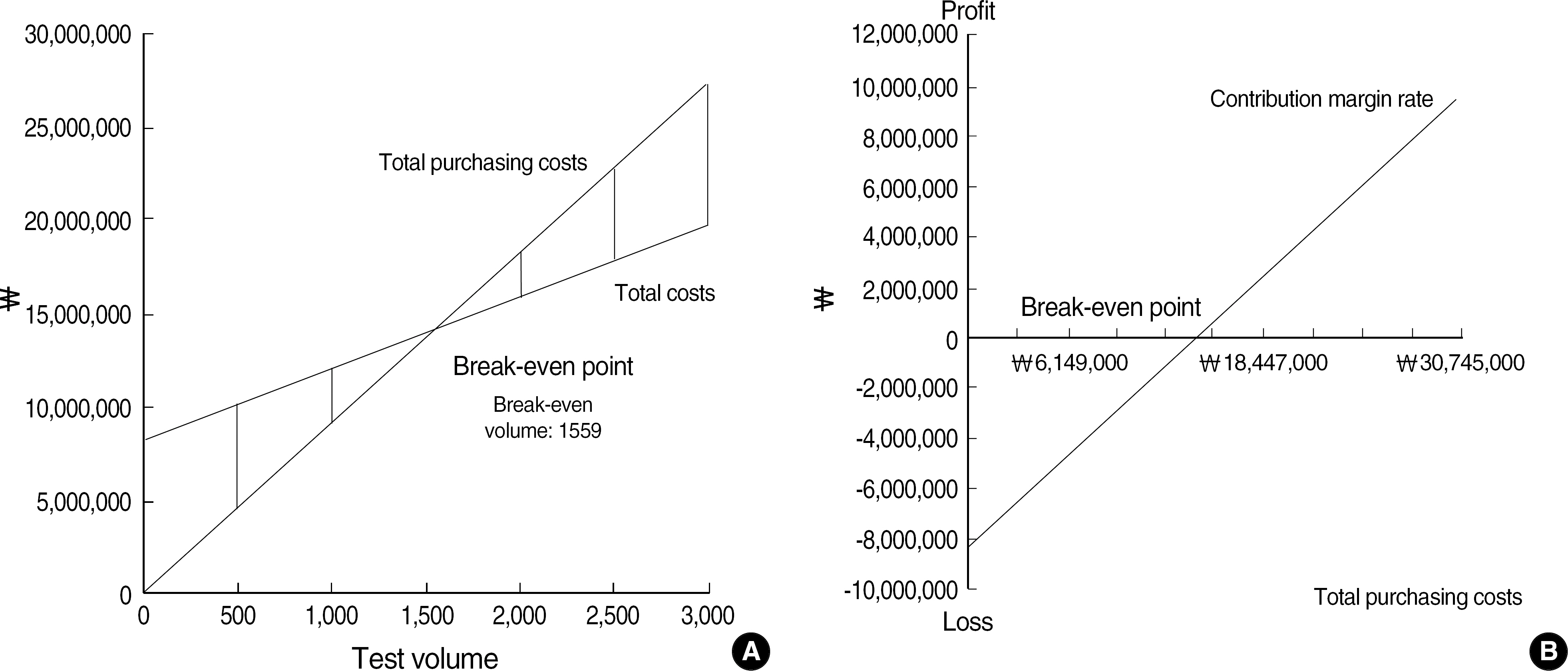

Fixed and variable costs were calculated in case that alpha fetoprotein (AFP), carcinoembryonic antigen (CEA), prostate-specific antigen (PSA), ferritin, free thyroxine (fT4), triiodothyronine (T3), thyroid-stimulating hormone (TSH), CA 125, CA 19-9, and hepatitis B envelope antibody (HBeAb) were to be tested with Abbott AxSYM instrument. Break-even volume was calculated as fixed cost per year divided by purchasing cost per test minus variable cost per test and BEP ratio as total purchasing costs at break-even volume divided by total purchasing costs at actual annual volume.

RESULTS

The average fixed cost per year of AFP, CEA, PSA, ferritin, fT4, T3, TSH, CA 125, CA 19- 9, and HBeAb was won 8,279,187 and average variable cost per test, won 3,786. Average break-even volume was 1,599 and average BEP ratio was 852%. Average BEP ratio without including quality costs such as calibration and quality control was 74%.

CONCLUSIONS

Because the quality assurance of clinical tests cannot be waived, outsourcing all of 10 items was more adequate than in-house make at the present volume in financial aspect. BEP analysis was useful as a financial tool for make-or-buy decision, the common matter which laboratory managers meet with.

MeSH Terms

-

alpha-Fetoproteins

Calibration

Carcinoembryonic Antigen

Cost Control

Ferritins

Hepatitis B

Immunoassay

Outsourced Services

Prostate-Specific Antigen

Quality Control

Quality Improvement

Thyrotropin

Thyroxine

Triiodothyronine

Carcinoembryonic Antigen

Ferritins

Prostate-Specific Antigen

Thyrotropin

Thyroxine

Triiodothyronine

alpha-Fetoproteins

Figure

-

Fig. 1. Fixed cost per test and variable test per test according to test volume change.

Fig. 2. Break-even chart (A) using total costs line and total purchasing costs line and (B) using contribution margin rate line.

Reference

-

References

1. Kim JQ, editor. Jo-en byungwon mandlgi. p. Seoul: Hangook–ehackwon. 2004. p. 3–7.2. Weiss RL, Ash KO. Laboratory management. Burtis CA, Ashwood ER, editors. Tietz textbook of clinical chemistry. 3rd ed.Philadelphia: WB Saunders;1999. p. 369–83.3. Westgard JO, Klee GG. Quality management. Burtis CA, Ashwood ER, editors. Tietz textbook of clinical chemistry. 3rd ed.Philadelphia: WB Saunders;1999. p. 384–418.4. National Committee for Clinical Laboratory Standards. Application of a quality management system model for laboratory services; Approved Guideline Third Edition. NCCLS. Document GP 26-A3.Wayne, PA: NCCLS;2004.5. National Committee for Clinical Laboratory Standards. Continuous Quality Improvement: Essential Management Approaches; Approved Guideline-Second Edition. NCCLS. Document GP 22-A2.Wayne, PA: NCCLS;2004.6. Horngren CT, editor. ed.Cost accounting. 10th ed.Seoul: Pearson education Korea;2003. p. 29–51.7. Higgins JM, editor. ed.Quantitative methods for problem solving and planning. In. Higgins JM, editor. The management challenge: an introduction to management. New York: Macmillan Publishing Company;1991. p. 209–43.8. Travers EM, Mcclatchey KD. Basic laboratory management. McClatchey KD, editor. ed.Clinical laboratory medicine. 2nd ed.Philadelphia: Lippincott Willams & Wilkins;2002. p. 3–48.9. Beard PL, Kerens EP, editors. eds.1st ed.How to negotiate capitation for laboratory services. Wachington D.C.: AACC, American Association for Clinical Chemistry, Inc.;1996. p. 9–14.10. Yang Namha, editor. ed.Sonikboongijumgwa hyungemhelm kyungyoung. 1st ed.Seoul: Sinrhonsa;2000. p. 59–145.11. National Committee for Clinical Laboratory Standards. Selecting and Evaluating a Referral Laboratory; Approved Guideline. NCCLS. Document GP 09-A.Wayne, PA: NCCLS;1998.12. National Committee for Clinical Laboratory Standards. Basic Cost Accounting for Clinical Services; Approved Guideline. NCCLS. Document GP 11-A.Wayne, PA: NCCLS;1998.

- Full Text Links

-

- Actions

-

Cited

- CITED

-

- Close

- Share

-

- Similar articles

-

- Comparisons of Test-Retest Reliability of Strength Measurement of Gluteus Medius Strength between Break and Make Test in Subjects with Pelvic Drop

- The clinical decision analysis using decision tree

- Medical decision making tools : Bayesian analysis and ROC analysis

- Public Health Nurses' Decision Making Models and Their Knowledge Structure

- Nurse's Conflict Experience toward End-of-life Medical Decision-making